Third Bi-Monthly Monetary Policy Statement on August 9, 2016 by Governor Rajan

Monetary Policy 2016-17

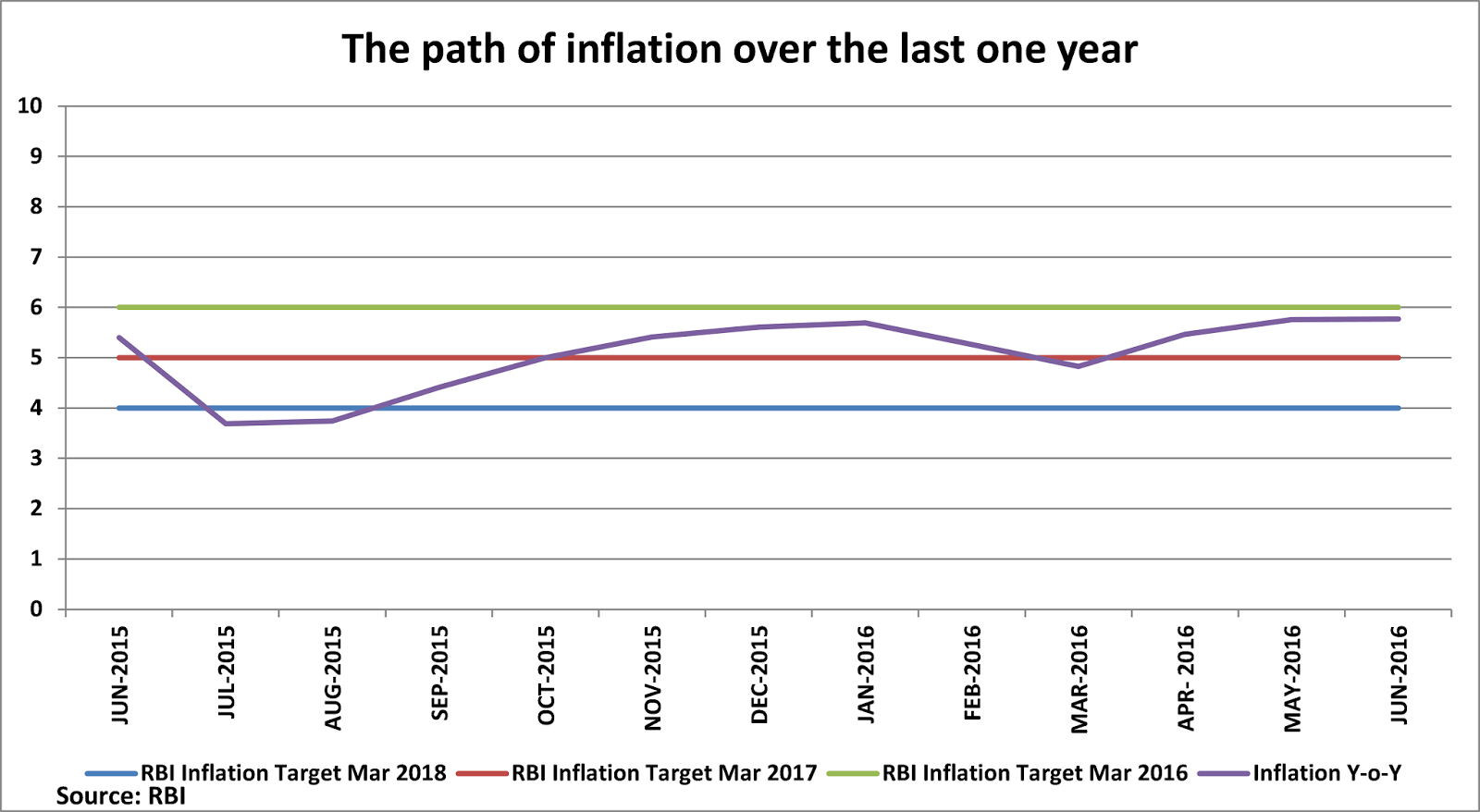

Governor Rajan in his statement indicated that the projected

trajectory of inflation for the rest of the year had moved higher: the culprit

– the recent higher than anticipated CPI inflation numbers led by higher food

prices. Yet strangely he expects no change in RBI’s inflation projection for March 2017: 5 %, with the risks on the upside.

Under normal circumstances, I would have said that the next

six months are likely to see little change in monetary policy.

But these are not normal times! First, Governor Rajan leaves

his position next month. Will the next Governor be as much inflation focussed

as the inflation obsessed – and rightly so - Rajan. Only time will tell.

Second, the Government is expected to announce the members

of the Monetary Policy Committee later this month. So at the October 4 monetary

policy statement, the verdict on the policy rate will be determined by the MPC,

not solely by the Governor.

Both these are huge changes in the environment, and could

lead to a sea change in interest rates. Currently, the guiding principle of

RBI’s thinking on the policy rate is that real rates should be positive, and

need to be about 1-1.5% positive. This explains why the repo rate is at 6.5%

against a projected inflation of 5% by March 2017, implying a real rate of 1.5%.

(To my mind there has been some weakening on this front by the RBI under

relentless government pressure.) Keeping real rates sufficiently positive is

key to India moving to a stable and lower inflation environment. Will MPC

members buy into RBI’s thinking?

It is difficult to say, but if the MPC does not buy into

RBI’s thinking then the repo rate could well come down by 0.50-0.75% to 5.75%

by March 2017, assuming inflation follows RBI’s projected path.

Industry leaders, consumers and investors will cheer, but

this may be short-lived. The credibility of India’s monetary policy may take a

significant hit, both in India and abroad, among knowledgeable central bank

watchers. Inflationary expectations may rise, and the stage may be set for a rise

in inflation, making the goal of 4% by March 2018 (+/- 2%) difficult l to

attain.