Fifth

Bi-Monthly Monetary Policy Statement, December 7, 2016

Monetary Policy 2016-17

Monetary Policy 2016-17

Not altogether a surprise that the

Monetary Policy Committee chose to keep the repo rate unchanged at 6.25%.

In my blog of November 25, 2016 on

the November 8 demonetisation of Rs. 500 and Rs. 1000 notes and the uncertainty it had

created for the growth of the economy in FY 2016-17, I had expressed the view that

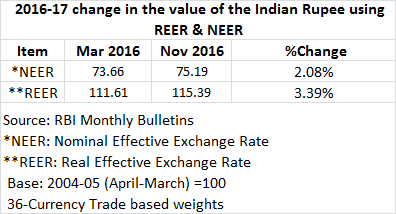

a reduction in the repo rate was likely, unless the rupee comes under

significant pressure. The rupee did come under significant pressure, falling at

one point by over 3% against the U.S. dollar since the last policy announcement

on October 4. In its outlook, the MPC noted that ‘U.S. monetary and fiscal

policy could impact volatility to the exchange rate thereby feeding into

inflation’ – the term ‘volatility’ being the RBI’s euphemism for weakness, in

my view.

Significantly, the RBI sees the

effects of demonetisation on the growth of the economy as purely ‘transient’.

In theory this is true as demonetisation is simply the substitution of one set

of notes by another happening without lag and friction.

Although, the RBI has reduced its growth

target for the year from 7.6% to 7.1%, in the words of the Executive Director

in the conference call with media, only 0.15% of the reduction is due to

demonetisation. The remaining 0.35% is due to the lower than expected number of

7.1% for growth in Q2 FY 2016-17. Perhaps the RBI feels that it has no hard

data points as yet on the effects of demonetisation on growth, despite the

widespread media reports about the difficulties faced by most sectors and

people in accessing cash, and the consequent slowdown in spending.

On the inflation front, there is no

change in RBI’s projected inflation path – 5% by March 2017, with risks to the

upside, although lower than the October policy review.

If this is the picture that the RBI

has of the economy for the rest of FY16-17, then its decision to make no change

in the repo rate is warranted. But is this picture correct? It is hard to

believe, at least based on media reports, that this is the case so far as the

growth of the economy is concerned. What about hard data points?

On December 9, the RBI released

fortnightly data on credit and deposits in the banking sector. In FY 2016-17

up to November 25, credit grew by just 0.6%! At the end of two quarters, i.e.

up to September 30, 2016, credit grew by 3.7%, less than the 4.2% seen in the same

period during the previous year.

So from September 30 to November 25, bank credit actually

fell - by Rs. 2,282 billion. Significantly most of that fall - Rs. 1672

billion - it appears happened even before the demonetisation on November 8!

On the inflation front, where RBI

did not have the benefit of hindsight, data was released just two days ago

which showed that consumer price inflation for November came in at 3.63%, well

below expectations. Does this suggest a softer inflation path than RBI’s

current one going into March 2017? Clearly one data point is not sufficient.

The RBI is in a wait and watch mode.

It is quite a surprise that at the

MPC meeting all members unanimously agreed that no change in the repo rate is

warranted.

Meanwhile, some banks have cut

their deposit rates and a few their lending rates.

One weakness with the MPC’s assessment and past statements is

that it does not show trends in bank credit and deposits, money supply and

reserve money on a

regular basis - even though the RBI is directly attempting to influence both

the price and flow of money in the economy through its monetary policy actions. This is necessary.