Accommodative

and neutral policy co-exist

Monetary

Policy 2016-17

The

key takeaways are the following:

Inflation in 2017-18 is expected to follow a

path of 4-4.5% in H1 and 4.5-5% in H2.

Growth for 2016-17 is revised downwards to

6.9% from 7.1%; growth in 2017-18 is expected to rebound from the temporary

effects of demonetisation to 7.4%.

Monetary policy shifts from an accommodating

stance to neutral.

There is some commitment by the RBI to bring

inflation closer to 4% (the earlier target to get to this March 2018 has been

given up), but there is no time frame. The predominant objective is 4%, with a

band of +/- 2% in a “medium term” sense (according to me March 2021 based on

the Government’s notification).

RBI wants banks to pass on more of the

reduction in the repo rate to customers – currently banks have passed on to

customers through a reduction in the lending rate about 0.85 % of the 1.75% cut

in the repo rate.

The band for the desired level of the real

interest rate now seems to have moved up from less than 1.5 % to 1.25-1.75.

There

are no surprises on the inflation and growth front. Recent inflation data

suggests that top line inflation is lower than was expected – for the last

three months CPI has been less than 4%. RBI expects inflation to pick in

FY17-18 back to its normal path, once the temporary deflationary impact of

demonetisation wears out.

At

the beginning of the financial year, I had predicted that RBI would reduce the

repo rate by 0.5%. This has happened, although I was wrong on the timing during

the financial year.

At

this bi-monthly statement, the last of FY17-18, RBI chose to keep the repo rate

unchanged. This is not a surprise.

With

inflation projected at about 5% or just below by end of FY17-18, and a target

real rate of 1.25-1.75%, a repo rate at 6.25% is appropriate.

What

is surprising is the RBI’s shift in monetary stance from accommodative to

neutral. While core inflation is about 5%, and there seems to be no let up on

this front – much of the recent fall in inflation is because of deflation in

vegetables and pulses (demonetisation effects of distress sales by farmers was

quoted by RBI) – RBI is concerned that the external factors may pose a risk to

inflation – in particular the volatility of the rupee. I had referred to this

in my blog of December 15, 2016 as a constraint on the RBI to further reduce

the repo rate, if it was felt necessary to do so to counteract larger than

expected temporary negative effects of demonetisation.

Some

evidence that inflation in the U.S. will rise to 2% , expectations of further

increases in the federal funds rate by the Federal Reserve, greater government

spending by the U.S. pushing the growth rate higher, can together loop back to

depreciate the rupee, which could lead to higher inflation in India.

Note

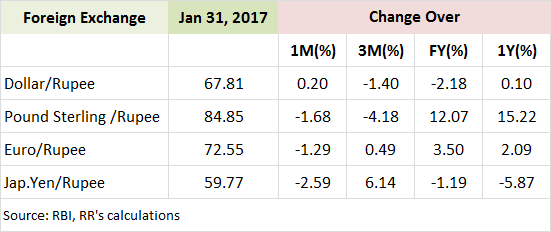

the rupee is arguably significantly overvalued. Please refer to my blog of

January 20, 2017 on this subject. It could be that if the scenario above

unfolds, RBI may let the rupee depreciate in an orderly manner. And why not:

growth needs to pick up at home, inflation is under control, and actively

preventing the rupee from falling could use up less foreign exchange reserves.

To

my mind, the underlying strong reason for the shift to a neutral monetary

stance is that RBI “requires further significant decline in inflationary

expectations” to push inflation below 5%. For this to happen, keeping real

rates at the top of its band for a considerable length of time in the current

environment is necessary. Hence a shift in its real interest band from the less

than 1.5% to 1.25 to 1.75% (please refer to the transcript of the conference

call with media). Under Governor Rajan, the real interest rate band was higher

at 1.5-2%. In this context, please read my blog of October 11, 2016.

Was

it necessary for the RBI to communicate a change in monetary stance? I would

have thought the MPC could have been silent on this issue. Banks may now

hesitate to reduce lending rates.

Where

does the repo rate go from here in 2017-18.?

To

my mind, if RBI’s projected path of inflation materialises in 2017-18, and RBI

sticks to its real interest rate stance, no change in the repo rate can be

expected till December. If some of the negative external factors (outlined

above) abate, then there is a possibility of a 0.25% reduction in the repo rate

in Q4 of 2017-18.