Thursday, 27 December 2018

Tuesday, 4 December 2018

RBI should keep the repo rate on hold in tomorrow's MPC statement

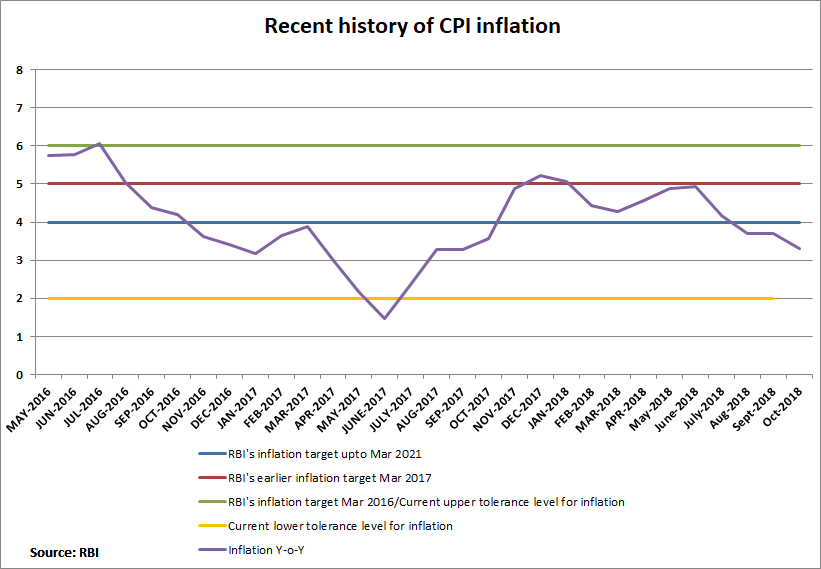

CPI Inflation for October fell further to 3.3%, the fourth month of consecutive decline, and for Q2 it has run below RBI's estimate of 4%. Oil prices have falled sharply over the last month. In this scenario, it is likely that the MPC will hold or even reduce the its H2 inflation forecast of 3.9-4.5%.

Even using the 4.5% number, the real rate, using the one year treasury bill, is in excess of 2.5%. This is far too high a real rate in this cycle. GDP growth for Q2 has come in at 7.1%, below RBI's estimate of 7.4%. It is now possible that RBI reduces its estimate of GDP growth of 7.4% in the full year 2018-19.

RBI needs to just stay the course and keep the repo rate at 6.5%.

Please see my earlier blogs on Monetary Policy.

Even using the 4.5% number, the real rate, using the one year treasury bill, is in excess of 2.5%. This is far too high a real rate in this cycle. GDP growth for Q2 has come in at 7.1%, below RBI's estimate of 7.4%. It is now possible that RBI reduces its estimate of GDP growth of 7.4% in the full year 2018-19.

RBI needs to just stay the course and keep the repo rate at 6.5%.

Please see my earlier blogs on Monetary Policy.

Monday, 3 December 2018

The value of the Rupee: update as of October 2018

REER falls to 110 area for the first time since April 2016: Rupee is in somewhat neutral territory.

Monitoring the Bull Market in Indian Stocks: Update as of November 2018

Please see my blog of July 9, 2014 for the original note on using TMV/GNP ratio to gauge whether the market is cheap or expensive, and my nonthly blogs on this subject.

Sunday, 2 December 2018

India Market Map: November 2018

Foreign Exchange

Subscribe to:

Comments (Atom)