Thursday, 27 December 2018

Tuesday, 4 December 2018

RBI should keep the repo rate on hold in tomorrow's MPC statement

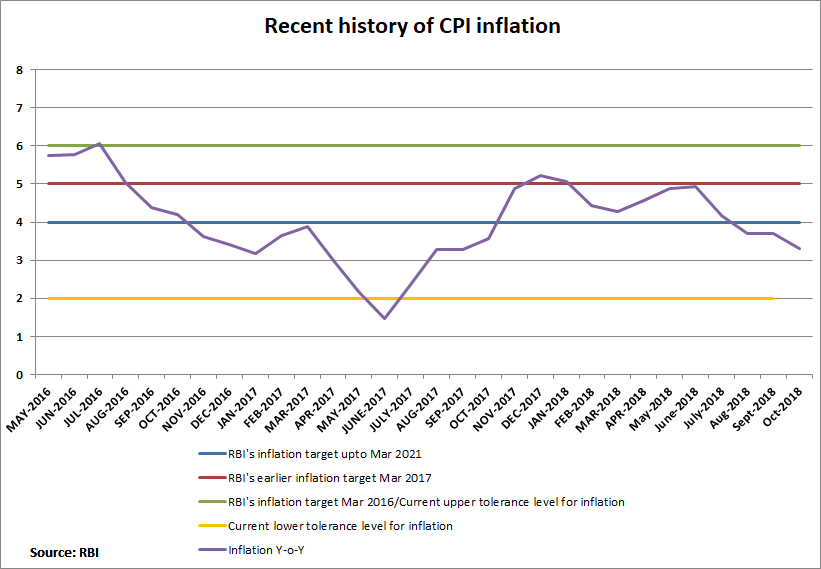

CPI Inflation for October fell further to 3.3%, the fourth month of consecutive decline, and for Q2 it has run below RBI's estimate of 4%. Oil prices have falled sharply over the last month. In this scenario, it is likely that the MPC will hold or even reduce the its H2 inflation forecast of 3.9-4.5%.

Even using the 4.5% number, the real rate, using the one year treasury bill, is in excess of 2.5%. This is far too high a real rate in this cycle. GDP growth for Q2 has come in at 7.1%, below RBI's estimate of 7.4%. It is now possible that RBI reduces its estimate of GDP growth of 7.4% in the full year 2018-19.

RBI needs to just stay the course and keep the repo rate at 6.5%.

Please see my earlier blogs on Monetary Policy.

Even using the 4.5% number, the real rate, using the one year treasury bill, is in excess of 2.5%. This is far too high a real rate in this cycle. GDP growth for Q2 has come in at 7.1%, below RBI's estimate of 7.4%. It is now possible that RBI reduces its estimate of GDP growth of 7.4% in the full year 2018-19.

RBI needs to just stay the course and keep the repo rate at 6.5%.

Please see my earlier blogs on Monetary Policy.

Monday, 3 December 2018

The value of the Rupee: update as of October 2018

REER falls to 110 area for the first time since April 2016: Rupee is in somewhat neutral territory.

Monitoring the Bull Market in Indian Stocks: Update as of November 2018

Please see my blog of July 9, 2014 for the original note on using TMV/GNP ratio to gauge whether the market is cheap or expensive, and my nonthly blogs on this subject.

Sunday, 2 December 2018

India Market Map: November 2018

Foreign Exchange

Wednesday, 7 November 2018

Fourth Bi-monthly Monetary Policy Statement of Ocotober 5 for 2018-19: RBI makes the right move by holding the repo rate steady

But policy stance change from neutral to tight is perhaps not the right move

RBI's projection for inflation for H2 of 2018-19 was lowered to a range of 3.9% - 4.5% from 4.8%, while the projection for the economy's growth rate was left unchanged at 7.4%.

Note that since the third bi-monthly monetary policy statement in June, inflation trended downwards in July and August to 4.17% and then 3.69%, the two data points RBI had before the fourth monetary policy statement on Ocotober 5th. (Since then the September inflation number has come further lower at 3.77%.)

My perception has been that there was no need for the RBI to have raised the repo rate by 0.5% in two steps in June and August this year. Please read my earlier blogs on this subject.

RBI's new policy stance means in Governor Patel's own words is that "there are only two options in this particular rate cycle, either we increase rates or keep them steady".

I had felt that the shift in RBI's stance from accommodative to neutral in February last year was too early, and the wrong signal then.

RBI's projection for inflation for H2 of 2018-19 was lowered to a range of 3.9% - 4.5% from 4.8%, while the projection for the economy's growth rate was left unchanged at 7.4%.

Note that since the third bi-monthly monetary policy statement in June, inflation trended downwards in July and August to 4.17% and then 3.69%, the two data points RBI had before the fourth monetary policy statement on Ocotober 5th. (Since then the September inflation number has come further lower at 3.77%.)

My perception has been that there was no need for the RBI to have raised the repo rate by 0.5% in two steps in June and August this year. Please read my earlier blogs on this subject.

RBI's new policy stance means in Governor Patel's own words is that "there are only two options in this particular rate cycle, either we increase rates or keep them steady".

I had felt that the shift in RBI's stance from accommodative to neutral in February last year was too early, and the wrong signal then.

Thursday, 1 November 2018

Monitoring the Bull Market in Indian Stocks: Update as of October 2018

Please see my blog of July 9, 2014 for the original note on using TMV/GNP ratio to gauge whether the market is cheap or expensive, and my nonthly blogs on this subject.

India Market Map: October 2018

Foreign Exchange

Stocks

Government Bonds

Gold

Money Market

Policy Rates

Bank Deposits

Public Provident Fund

Post Office

Home Loans

Real Estate

Wednesday, 31 October 2018

The flow of money up to Q2 2018-19 : trend continues

Pick up in credit growth extends - deposit growth weak

Deposit and credit growth

Please see my earlier blog on this subject.

The tables below give the picture over the last one year. Let's look at it using another time frame also.

In the last two years (Sept. over Sept., 2016-17 and 2017-18) covering demonetisation and GST, deposit growth fell to 8.4% from the earlier two years (Sept. over Sept., 2014-15 and 2016-17) number of 11.3% - a very sharp fall.

Credit grow in the last two years (Sept. over Sept., 2016-17 and 2017-18) covering demonetisation and GST is now about the same level as compared to the earlier two years (Sept. over Sept., 2014-15 and 2016-17) number of 10%. So although there is a pick-up in credit growth in the last year, as seen in the table below, it is over a two year period just a return to normalcy.

Money Supply

Instead of looking at just the last year, as in the case of bank deposits and credits, let's look at a longer time frame.

In the last two years (Sept. over Sept., 2016-17 and 2017-18) covering demonetisation and GST, money supply growth fell to 8 % from the earlier two years (Sept. over Sept., 2014-15 and 2016-17) number of 11.5% - a sharp fall. Normally a central bank, including the RBI, targets to grow money supply in the same order as the nominal growth of the economy.

Deposit and credit growth

Please see my earlier blog on this subject.

The tables below give the picture over the last one year. Let's look at it using another time frame also.

In the last two years (Sept. over Sept., 2016-17 and 2017-18) covering demonetisation and GST, deposit growth fell to 8.4% from the earlier two years (Sept. over Sept., 2014-15 and 2016-17) number of 11.3% - a very sharp fall.

Credit grow in the last two years (Sept. over Sept., 2016-17 and 2017-18) covering demonetisation and GST is now about the same level as compared to the earlier two years (Sept. over Sept., 2014-15 and 2016-17) number of 10%. So although there is a pick-up in credit growth in the last year, as seen in the table below, it is over a two year period just a return to normalcy.

Instead of looking at just the last year, as in the case of bank deposits and credits, let's look at a longer time frame.

In the last two years (Sept. over Sept., 2016-17 and 2017-18) covering demonetisation and GST, money supply growth fell to 8 % from the earlier two years (Sept. over Sept., 2014-15 and 2016-17) number of 11.5% - a sharp fall. Normally a central bank, including the RBI, targets to grow money supply in the same order as the nominal growth of the economy.

Reserve Money

Tuesday, 30 October 2018

The value of the Rupee: update as of September 2018

From its peak in January, the rupee has fallen sharply on a real basis

Below the usual monthly tables on the rupee.

On another note, the rupee's real effective exchange rate (REER) peaked in January this year at 122. Up to September, using this measure the rupee has fallen by 9%. On a noninal effective exchange rate (NEER) basis, the rupee has fallen by 7% during the same period.

Thursday, 18 October 2018

Monday, 1 October 2018

Monitoring the Bull Market in Indian Stocks: Update as of September 2018

Please see my blog of July 9, 2014 for the original note on using TMV/GNP ratio to gauge whether the market is cheap or expensive, and my nonthly blogs on this subject.

India Market Map: September 2018

Foreign Exchange

Money Market

Subscribe to:

Comments (Atom)